Conforming Dreams: A Verse on Mortgage Realities

Conforming Dreams: A Verse on Mortgage Realities

Introduction to Conforming Mortgages

In the world of real estate financing, conforming mortgages play a pivotal role in enabling countless individuals to achieve their dreams of homeownership. But what exactly is a conforming mortgage? Essentially, it’s a type of loan that meets the criteria set forth by government-sponsored enterprises (GSEs) such as Fannie Mae and Freddie Mac. These loans adhere to specific guidelines regarding loan size, borrower creditworthiness, and other factors deemed crucial for mortgage eligibility.

Qualifying for a Conforming Mortgage

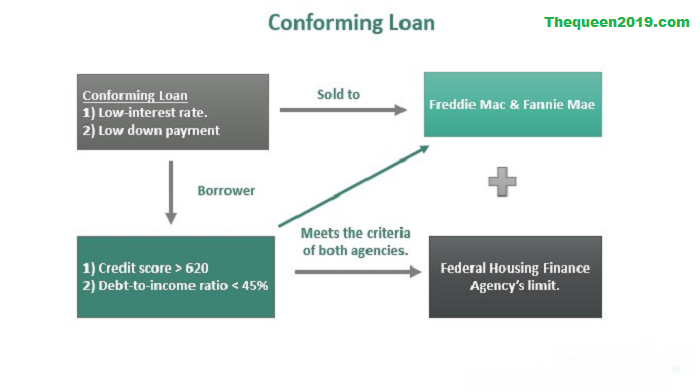

One of the primary considerations when applying for a conforming mortgage is meeting the qualification criteria. Lenders typically assess several factors, including the applicant’s credit score, debt-to-income ratio, and down payment capability. While the exact requirements may vary from one lender to another, borrowers are generally expected to have a decent credit score, a manageable level of debt, and the ability to make a down payment, albeit the amount may vary.

Benefits of Conforming Mortgages

One of the most enticing aspects of conforming mortgages is their favorable interest rates. Since these loans are considered less risky by lenders due to their adherence to established guidelines, borrowers often enjoy lower interest rates compared to non-conforming loans. Additionally, the qualification process for conforming mortgages tends to be more streamlined and less stringent, making it easier for borrowers to secure financing for their home purchases. Moreover, conforming mortgages often come with higher loan limits, allowing borrowers to finance more expensive properties.

Understanding Conforming Loan Limits

Conforming loan limits refer to the maximum amount of money that lenders can lend to borrowers while still conforming to the guidelines set by GSEs. These limits vary depending on factors such as the location of the property and the type of loan. In areas with higher housing costs, loan limits are typically higher, reflecting the increased cost of homeownership in such regions. For borrowers, conforming loan limits determine the maximum amount they can borrow to purchase a home within the confines of a conforming mortgage.

Comparison with Non-Conforming Mortgages

While conforming mortgages adhere to strict guidelines set by GSEs, non-conforming mortgages, also known as jumbo loans, do not. Non-conforming loans exceed the maximum loan limits established by GSEs or deviate from other eligibility criteria, making them riskier for lenders. As a result, borrowers seeking non-conforming mortgages may encounter stricter qualification requirements and higher interest rates compared to their conforming counterparts.

The Role of Government-Sponsored Enterprises (GSEs)

Fannie Mae and Freddie Mac, two prominent GSEs, play a crucial role in the conforming mortgage market by purchasing conforming loans from lenders and providing liquidity to the mortgage industry. By doing so, they facilitate the flow of funds from investors to borrowers, thereby ensuring the availability of affordable mortgage financing to a wide range of individuals. The activities of these GSEs have a profound impact on both borrowers and lenders, influencing the availability and cost of mortgage credit in the market.

Risks and Considerations

While conforming mortgages offer numerous benefits, they are not without risks. Market fluctuations, for instance, can affect interest rates and housing affordability, potentially impacting borrowers’ ability to repay their loans. Additionally, some conforming mortgages may come with prepayment penalties or other hidden costs that borrowers should be aware of before committing to a loan.

Tips for Choosing a Conforming Mortgage

When shopping for a conforming mortgage, it’s essential to do your homework and carefully evaluate your options. Researching different lenders, understanding the terms and conditions of various loan products, and seeking advice from mortgage professionals can help you make an informed decision that aligns with your financial goals and circumstances.

The Application Process

The process of applying for a conforming mortgage typically involves several steps, including completing a loan application, providing documentation to verify your income and assets, undergoing a credit check, and obtaining pre-approval from the lender. Once approved, the loan will undergo final underwriting before funds are disbursed to complete the purchase transaction.

Common Misconceptions

Despite their widespread use, conforming mortgages are often subject to misconceptions and misunderstandings. Some people believe, for example, that conforming mortgages are only available to borrowers with pristine credit histories, while others may mistakenly assume that conforming loans are limited to primary residences. Dispelling these myths and addressing common concerns can help borrowers make more informed decisions about their financing options.

The Impact of Conforming Mortgages on the Real Estate Market

The availability of conforming mortgages plays a significant role in shaping the dynamics of the real estate market. By providing affordable financing options to a broad spectrum of homebuyers, conforming mortgages contribute to housing affordability and market stability. Additionally, the liquidity provided by GSEs ensures that lenders have access to the funds needed to originate new loans, further stimulating housing activity and economic growth.

Case Studies and Examples

Real-life examples of individuals benefiting from conforming mortgages abound. From first-time homebuyers achieving their homeownership dreams to seasoned investors expanding their real estate portfolios, conforming mortgages have empowered countless individuals to pursue their housing goals. While success stories are prevalent, challenges such as market fluctuations and changing regulatory environments underscore the importance of careful planning and due diligence when navigating the mortgage landscape.

Future Trends in Conforming Mortgages

Looking ahead, several trends are poised to shape the future of the conforming mortgage market. Technological advancements, for instance, may streamline the mortgage application process and enhance the borrower experience. Regulatory changes, on the other hand, could impact lending standards and eligibility criteria, influencing the availability and cost of conforming mortgages. By staying informed and adapting to evolving market conditions, borrowers can position themselves for success in the ever-changing world of real estate finance.

Conclusion

In conclusion, conforming mortgages serve as a cornerstone of the real estate industry, providing affordable financing options to a diverse range of borrowers. By adhering to established guidelines and leveraging the support of government-sponsored enterprises, these loans enable countless individuals to achieve their homeownership dreams and build wealth through real estate. While not without risks and challenges, conforming mortgages offer numerous benefits that make them a popular choice for homebuyers across the country.

FAQs

What are the advantages of a conforming mortgage?

Conforming mortgages typically offer lower interest rates, easier qualification criteria, and higher loan limits compared to non-conforming loans, making them an attractive option for many borrowers.

How does the conforming loan limit affect borrowers?

The conforming loan limit determines the maximum amount that borrowers can borrow under a conforming mortgage. Exceeding this limit may necessitate obtaining a non-conforming or jumbo loan, which often comes with stricter requirements and higher interest rates.

Can I qualify for a conforming mortgage with a low credit score?

While a higher credit score may improve your chances of qualifying for a conforming mortgage and securing favorable terms, lenders consider various factors when evaluating loan applications, including income, debt-to-income ratio, and employment history.

Are conforming mortgages available for investment properties?

Conforming mortgages are primarily intended for owner-occupied properties, such as primary residences and second homes. Financing options for investment properties may differ, typically requiring larger down payments and stricter qualification criteria.

What happens if I default on a conforming mortgage?

Defaulting on a conforming mortgage can have serious consequences, including foreclosure proceedings initiated by the lender. It’s essential to communicate with your lender if you encounter financial difficulties to explore potential options for avoiding default and mitigating the impact on your credit.