Understanding Your Personal Loan Options, Factors to Take Into Account, and Techniques for Reliability and Financial Well-Being

Personal loans are flexible financial instruments that enable people to get capital for a range of reasons, including debt relief, home upgrades, significant purchases, or unforeseen costs. To maintain financial well-being, navigating the personal loan market necessitates having a solid grasp of the options accessible, important factors, and responsible borrowing techniques. This in-depth manual seeks to examine the realm of personal loans by providing information on various loan choices, crucial elements to take into account, and useful techniques for successfully handling personal loan debt.

Personal Loan Types

Personal loans are an adaptable financial instrument that can be utilized for a number of things, including home improvement and debt consolidation. People can select the best personal loan choice depending on their financial circumstances and objectives by being aware of the various sorts that are accessible. These are a few typical categories of personal loans:

1. Protected Individual Loans:

A vehicle, house, or savings account serves as collateral for secured personal loans.

Because collateral lowers the lender’s risk, secured loans are usually easier to qualify for and have lower interest rates.

The lender may take possession of the collateral to satisfy the outstanding balance if the borrower defaults on the loan.

2. Unsecured Individual Loans:

Collateral is not needed for unsecured personal loans; instead, the borrower’s creditworthiness is the only consideration.

Because unsecured loans pose a greater risk to lenders, they could have more stringent approval requirements and higher interest rates.

Approval for unsecured personal loans is more likely for borrowers with high credit ratings.

3. Fixed-Rate Individual Loans:

Fixed-rate personal loans yield regular monthly payments because their interest rate is constant for the duration of the loan.

Because they know exactly how much they must pay each month, borrowers can budget more easily and with predictability.

For people who would rather have certainty over fluctuating interest rates, fixed-rate loans are the best option.

4. Personal Loans with Variable Rates:

Interest rates on personal loans with variable rates are subject to alter over time in response to changes in the market.

Although starting rates might be less than for fixed-rate loans, there is a chance that they would rise, which would raise monthly payments for borrowers.

If lower interest rates are anticipated in the future, variable-rate loans may be favorable.

5. Loans for Debt Consolidation:

Credit card balances and medical expenses are examples of the kinds of obligations that can be consolidated into a single loan via debt consolidation loans.

Debt consolidation allows consumers to handle their payments more easily, simplify their finances, and possibly even cut their interest rates.

Loans for debt consolidation can reduce interest costs and help borrowers pay off high-interest debt more quickly.

6. Loans for Home Improvement:

Loans for home improvement are intended to pay for upgrades, repairs, and renovations.

These loans can be used for essential repairs, to improve energy efficiency, or to raise the value of a house.

Depending on the lender and the amount borrowed, home renovation loans can be either secured or unsecured.

7. Short-Term Loans:

Fast access to money is made possible by emergency loans for unforeseen costs such urgent home repairs, auto repairs, or medical fees.

These loans may be accessible to consumers with less-than-perfect credit and usually have quick approval procedures.

In times of need, emergency loans can assist people in covering unforeseen expenses and avoiding financial hardship.

Important Things to Think About Before Getting a Personal Loan

To make sure that borrowing is a responsible and advantageous move, it is crucial to thoroughly review your financial status, determine your borrowing needs, and take into account a number of other aspects before taking out a personal loan. Prior to submitting an application for a personal loan, bear the following points in mind:

1. Evaluate Your Cash Position:

To ascertain whether you can afford to take on more debt, evaluate your income, spending, and current debt.

Determine the monthly amount that you can comfortably borrow and repay without putting too much strain on your budget.

2. Explain Why You Are Borrowing:

Indicate in detail why you’re taking out a personal loan, including emergencies, big expenditures, home renovations, and debt consolidation.

Make sure the loan amount is in line with your particular financial objectives and refrain from taking on more debt than you need.

3. Verify Your Credit Rating:

To determine your creditworthiness, get a copy of your credit report and look up your credit score.

You can be eligible for better loan arrangements, such as lower interest rates and larger loan amounts if your credit score is higher.

4. Evaluate Loan Offers and Lenders:

To compare interest rates, costs, and terms, do your homework on several lenders, such as banks, credit unions, and online lenders.

Select a trustworthy lender that offers competitive rates and good loan terms that meet your demands financially.

5. Comprehend the terms and fees of the loan:

To fully comprehend all terms and conditions, including the interest rate, repayment timeline, and any associated costs, thoroughly read the loan agreement.

Be mindful of the origination, prepayment, and late payment costs as these might affect the overall cost of borrowing.

6. Examine Secured vs. Unsecured Credit:

Determine if an unsecured or secured personal loan is better for your financial circumstances.

While unsecured loans do not require collateral but may have higher interest rates, secured loans may have lower rates but do require collateral.

7. Examine Your Repayment Options:

After taking into account the total interest paid over the loan duration as well as the monthly payment amount, choose the loan term that best suits your needs.

To expedite the payback process and prevent missed payments, look into options like autopay or biweekly installments.

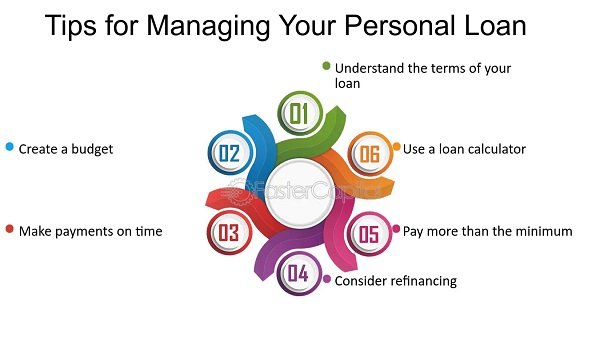

8. Debt Repayment Strategy:

To guarantee loan payback on time, create a repayment schedule that fits into your spending strategy and financial objectives.

Include the monthly loan payment in your spending plan, and give punctual payments top priority to prevent late fines and damage to your credit report.

9. If Needed, Seek Financial Advice:

See a credit counselor or financial advisor if you are unsure about taking out a personal loan or if you need help handling your money.

You can create a customized financial strategy for reaching your objectives and make well-informed borrowing selections with the assistance of professional advice.